The first implementation phase for CSRD is now beginning

January 16, 2024

As of January 1, 2024, the CSRD (Corporate Sustainability Reporting Directive) began to apply to the first group of affected companies, thereby replacing the previous NFRD (Non-Financial Reporting Directive) directives that have been in effect since 2014. Here we have gathered the most important facts about the new directive.

CSRD was adopted in November 2022 and entered into force in January 2023. The directive is one of the cornerstones of the European Green Deal and the sustainable finance agenda. The purpose of CSRD is to address the shortcomings of NFRD, which laid the foundation for the EU's mandatory sustainability reporting, and to introduce more detailed reporting requirements on companies' social and environmental impact. In addition, CSRD greatly expands the number of companies that must comply with the legislation – from approximately 11,700 covered by NFRD to almost 50,000.

CSRD's implementation phases

As mentioned, CSRD's reporting requirements began to apply for financial years starting on or after January 1, 2024, but this is only the first phase in CSRD's timeline. Different groups of companies will be gradually covered by the legislation in four stages:

1. Sustainability reporting with data from 2024 to be published in 2025

Companies already covered by NFRD, i.e. large listed companies, large banks and large insurance companies in the EU if they all have more than 500 employees, as well as companies outside the EU with securities listed on regulated markets in the EU and more than 500 employees.

2. Sustainability reporting with data from 2025 to be published in 2026

Other EU companies and companies outside the EU with securities listed on regulated markets in the EU that meet at least two of three of the Accounting Directive's* criteria for large companies: a) net turnover of more than EUR 50 million; b) balance sheet of more than EUR 25 million; c) average number of employees greater than 250.

3. Sustainability reporting with data from 2026 to be published in 2027

However – these companies can choose to postpone reporting for an additional two years, so the latest possible year to publish the first report should be 2029 with data from 2028

Small and medium-sized enterprises both from and outside the EU with securities listed on regulated markets in the EU; The Accounting Directive* defines small and medium-sized enterprises as companies that do not exceed at least two criteria for large companies and that exceed at least two criteria for micro-enterprises: a) net turnover of more than EUR 900,000; b) balance sheet of more than EUR 450,000; c) average number of employees greater than 10.

4. Sustainability reporting with data from 2028 to be published in 2029 and reporting at group level

Companies outside the EU with a turnover of more than EUR 150 million per year in the EU and which in the EU have either a branch with a turnover of more than EUR 40 million or a subsidiary which, according to the Accounting Directive*, is a large company or a listed small or medium-sized company.

*adjusted for 25% inflation according to the recently adopted delegated directive

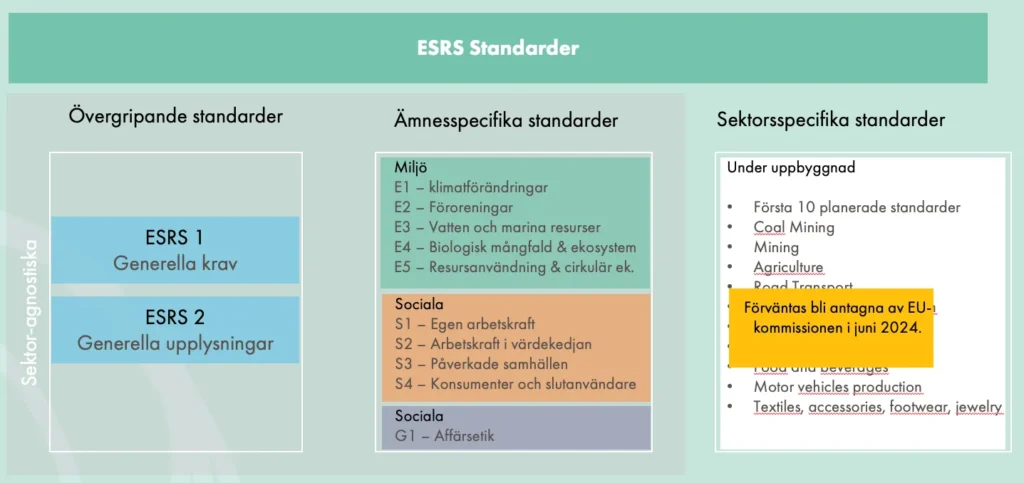

ESRS

All reporting requirements under CSRD are gathered in sustainability reporting standards called ESRS (European Sustainability Reporting Standards) developed by EFRAG (European Financial Reporting Advisory Group), a private association formed with the support of the European Commission.

ESRS are divided into the following categories:

All overarching and topic-specific standards were adopted in July 2023, while sector-specific standards were planned to be adopted by the end of June 2024. However, according to a new proposal published together with the Commission's work program for 2024, the EU Commission aims to postpone the adoption of sector-specific ESRS by two years to ensure that EFRAG has time to develop effective sector-specific standards.

Regarding overarching standards, ESRS 1 provides an understanding of the structure of ESRS, the basic concepts used in standards, and the general requirements for preparing and presenting sustainability information. ESRS 2, in turn, establishes disclosure requirements for the information that the company must provide on all material sustainability issues.

Since ESRS 1 does not contain any disclosure requirements, ESRS 2 is the only mandatory standard. However, not all topic-specific standards are voluntary, but subject to a materiality analysis that is intended to be the starting point for reporting according to ESRS. This means that companies only need to report information that is deemed material to their operations.

Double materiality

A sustainability issue is material when it meets the criteria for one or both dimensions of double materiality, i.e., impact materiality and financial materiality. Impact materiality concerns the company's actual or potential negative and positive impact on people or the environment in its own operations and in the value chain. On the other hand, financial materiality includes risks or opportunities that have or can be expected to have a significant impact on the company's development and its financial performance.

If a company concludes that one of the sustainability issues is not material and therefore omits all disclosure requirements related to that topic, the company will need to provide a brief explanation of the conclusions from its materiality analysis for that issue. This applies to all topic-specific standards except ESRS E1 Climate Change. For this standard, companies need to provide a detailed explanation of the conclusions from the materiality analysis, including a forward-looking analysis of the conditions that could lead the company to conclude that climate change is material in the future. Climate change is thus prioritized as a sustainability topic due to its comprehensive and systematic effects throughout the economy.

CSRD-adapted reporting in Our Impacts

Our Impacts, the Sustainability Platform that ZeroMission has offered its customers since 2011, is specially adapted for calculating companies' emissions as required by ESRS E1 but can also handle other sustainability factors. Since the platform is also built to be verified by third parties, it meets CSRD's requirements for third-party review.

Feel free to contact us directly if you want to know more about climate calculations with Our Impacts.

Read more about CSRD reporting in Our Impacts with our seminar.

Or see an introduction to how ZeroMission's digital platform can be used together with Knowit.